Crypto Investments: The New Path to Wealth for U.S.-Listed Companies

On May 27, a little-known stock caused a huge wave in the Nasdaq trading hall.

SharpLink Gaming (SBET), a small gambling company with a market capitalization of only $10 million, announced that it acquired approximately 163,000 Ethereum (ETH) through a $425 million private equity investment.

As soon as the news broke, SharpLink’s stock price skyrocketed, with an increase of over 500% at one point.

Buying coins may be becoming the new wealth code for publicly listed companies in the US stock market to boost their stock prices.

The source of the story is naturally MicroStrategy (now renamed Strategy, stock code MSTR), the company that first ignited the flames of battle, which boldly bet on Bitcoin as early as 2020.

In five years, it has transformed from an ordinary tech company into a “Bitcoin investment pioneer.” In 2020, MicroStrategy’s stock price was just over $10; by 2025, the stock had soared to $370, with a market capitalization exceeding $100 billion.

Buying coins not only inflated MicroStrategy’s balance sheet but also made it a darling of the capital markets.

In 2025, this craze will become more intense.

From tech companies to retail giants, and even to small gambling enterprises, US-listed companies are igniting a new engine of valuation with cryptocurrency.

What is the secret behind making wealth by buying coins to increase market value?

MicroStrategy, a textbook on the integration of coin and stock play.

It all started with MicroStrategy.

In 2020, this enterprise software company was the first to ignite the craze of buying coins in the US stock market, and CEO Michael Saylor stated that Bitcoin is a “more reliable store of value than the dollar”;

The charging faith is exciting, but what really sets this company apart is its play in the capital market.

MicroStrategy’s strategy can be summarized as a combination of “convertible bonds + Bitcoin:”

First, the company raises funds by issuing low-interest convertible bonds.

Since 2020, MicroStrategy has issued such bonds multiple times, with interest rates as low as 0%, far below the market average. For example, in November 2024, it issued $2.6 billion in convertible bonds, with a financing cost of almost zero.

These bonds allow investors to convert them into company stock at a fixed price in the future, equivalent to giving investors a call option, while enabling the company to obtain cash at a very low cost.

Secondly, MicroStrategy will invest all the raised funds into Bitcoin. By continuously increasing their Bitcoin holdings through multiple rounds of financing, Bitcoin has become a core component of the company’s balance sheet.

Finally, MicroStrategy leveraged the premium effect brought by the rise in Bitcoin prices to initiate a “flywheel effect”.

When the price of Bitcoin rose from $10,000 in 2020 to $100,000 in 2025, the company’s asset value increased significantly, attracting more investors to buy its stock. The rise in stock prices allowed MicroStrategy to issue bonds or stocks again at a higher valuation, raising more funds to continue purchasing Bitcoin, thus creating a self-reinforcing capital cycle.

The core of this model lies in the combination of low-cost financing and high-return assets. By borrowing money through convertible bonds at nearly zero cost, buying volatile but long-term bullish bitcoin, and then leveraging the market’s enthusiasm for cryptocurrency to amplify valuations.

This approach not only changed MicroStrategy’s asset structure, but also provided a textbook example for other US stock companies.

SharpLink, the meaning of borrowing a shell is not in the wine.

SharpLink Gaming (SBET) has optimized the above gameplay, using Ethereum (ETH) as the asset instead of Bitcoin.

But behind this, there is a clever combination of the power of the coin circle and the capital market.

Its gameplay can also be summarized as “backdoor listing”, with the core being to leverage the “shell” of a listed company and the cryptocurrency narrative to quickly amplify the valuation bubble.

SharpLink was originally a small company struggling on the verge of being delisted from NASDAQ, with its stock price dropping below $1, shareholders’ equity of less than $2.5 million, and immense compliance pressure.

But it has a trump card - the listing status of Nasdaq.

This “shell” has attracted the attention of big players in the coin circle: ConsenSys, led by Ethereum co-founder Joe Lubin.

In May 2025, ConsenSys, in collaboration with several venture capital firms in the cryptocurrency sector (such as ParaFi Capital and Pantera Capital), led the acquisition of SharpLink through a $425 million PIPE (Private Investment in Public Equity).

They issued 69.1 million new shares (at $6.15 per share), quickly acquiring over 90% control of SharpLink, bypassing the cumbersome process of an IPO or SPAC. Joe Lubin was appointed as the chairman of the board, and ConsenSys clearly stated that it will collaborate with SharpLink to explore the “Ethereum treasury strategy.”

Some say this is the ETH version of MicroStrategy, but in reality, the gameplay is more sophisticated.

The real purpose of this transaction is not to improve the gambling business of SharpLink, but rather for it to become a stronghold for the cryptocurrency sector to enter the capital market.

ConsenSys plans to purchase approximately 163,000 ETH with the 425 million USD, packaging it as the “Ethereum version of MicroStrategy,” and claims that ETH is a “digital reserve asset.”

The capital market is about “story premium”; this narrative not only attracts speculative funds but also provides an “open ETH proxy” for institutional investors who cannot directly hold ETH.

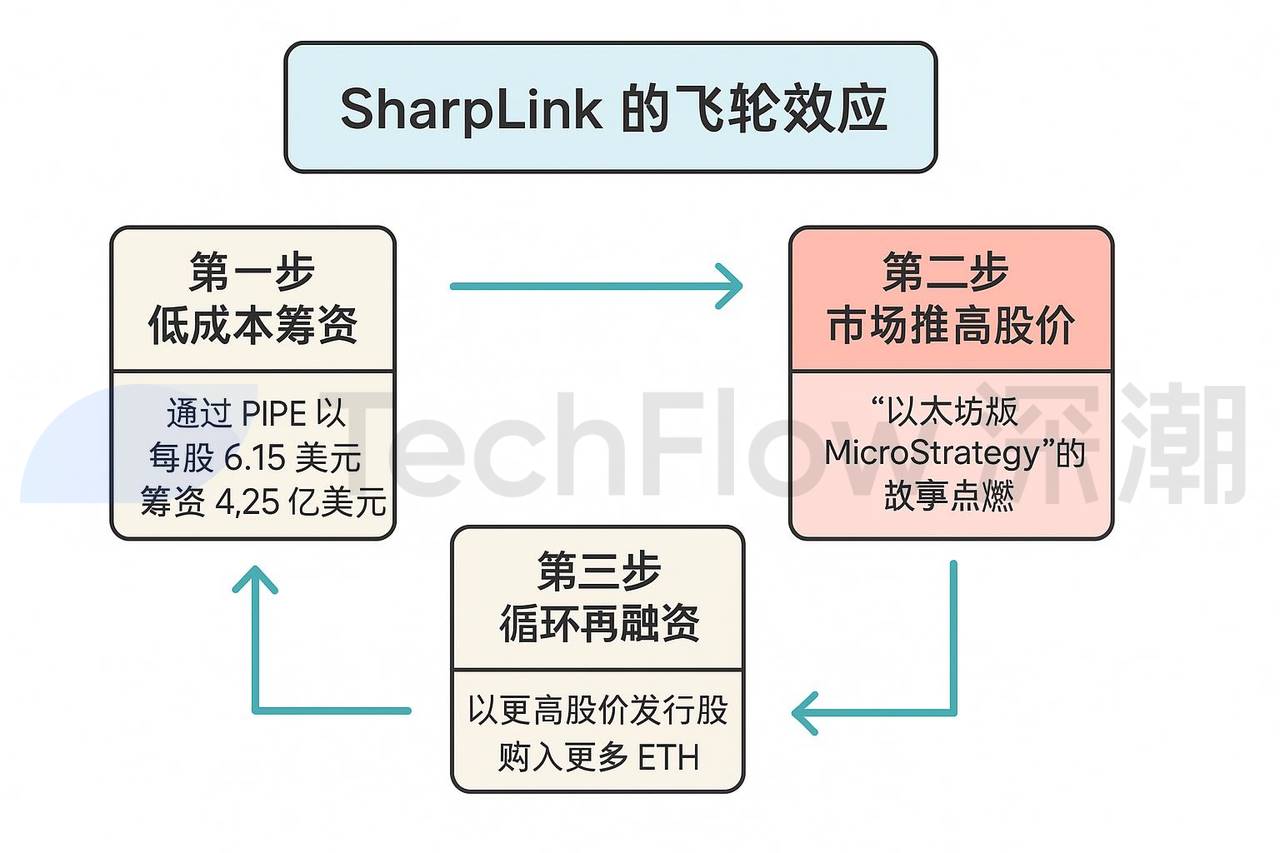

Buying coins is just the first step; the real “magic” of SharpLink lies in the flywheel effect. Its operation can be broken down into a three-step cycle:

The first step is low-cost fundraising.

SharpLink raised $425 million through PIPE at a price of $6.15 per share, which eliminates the cumbersome roadshows and regulatory processes required by IPOs or SPACs, resulting in lower costs.

Step two, market enthusiasm drives up stock prices.

Investors are ignited by the story of the “Ethereum version of MicroStrategy,” and the stock price has skyrocketed. The market’s enthusiasm for SharpLink stock far exceeds its asset value, with investors willing to pay prices much higher than its net value of ETH holdings, creating a “psychological premium” that rapidly inflates SharpLink’s market capitalization.

SharpLink also plans to stake these ETH coins, locking them in the Ethereum network, while earning an annual yield of 3%-5%.

Step three, cyclical refinancing. By issuing stocks again at a higher stock price, SharpLink can theoretically raise more funds, buy more ETH, and repeat the cycle, with the valuation growing larger like a snowball.

Behind this “capital magic,” there lies the shadow of a bubble.

SharpLink’s core business - gambling marketing - is almost neglected, and the $425 million ETH investment plan is completely disconnected from its fundamentals. Its stock price has soared, driven more by speculative funds and the crypto narrative.

The truth is that capital in the coin circle can also quickly inflate valuation bubbles through the “shell borrowing + buying coins” model, utilizing some small and medium-sized listed companies’ shells.

The intention of the drunken man is not in the wine; it is naturally good if the listed company’s business is related, but if it is not related, it is actually not important.

Imitation is not foolproof.

The strategy of buying coins seems to be the “wealth code” for listed companies in the US stock market, but it is not foolproof.

On the road of imitation, it is crowded with latecomers.

On May 28, GameStop, the game retail giant that became famous for the retail investor battle against Wall Street, announced that it had purchased 4,710 bitcoins for $512.6 million, attempting to replicate MicroStrategy’s success. However, the market reacted coldly: after the announcement, GameStop’s stock price fell by 10.9%, and investors were not convinced.

On May 15, Addentax Group Corp (stock code ATXG), a Chinese textile and apparel company, announced plans to acquire 8,000 Bitcoins and Trump’s TRUMP coin by issuing common stock. Based on the current Bitcoin price of $108,000, this purchase cost will exceed $800 million.

However, in contrast, the company’s total stock market value is only about 4.5 million dollars, which means its theoretical coin acquisition cost is more than 100 times the company’s market value.

Almost at the same time, another Chinese company listed on the US stock market, Jiuzi Holdings (stock code JZXN), also joined this coin buying craze.

The company announced plans to purchase 1,000 coins in Bitcoin over the next year, at a cost of over 100 million dollars.

Public information shows that Jiuzhi Holdings is a Chinese company focused on the retail of new energy vehicles, established in 2019. The company’s retail stores are mainly located in China’s third and fourth-tier cities.

The total market capitalization of this company on Nasdaq is only about 50 million dollars.

The stock price is indeed rising, but the matching degree between the company’s market value and the cost of buying coins is key.

For more latecomers, if the price of Bitcoin falls and they really buy in, their balance sheets will face immense pressure.

Buying coin strategies are not a universal wealth code. Lack of fundamental support and overly leveraged coin buying gambles may just be a risky path to a bubble burst.

Another way to break out

Despite the numerous risks, the buying craze for coins still has the potential to become the new normal.

In 2025, global inflation pressures and expectations of US dollar depreciation continue, and more and more companies are beginning to view Bitcoin and Ethereum as “inflation-resistant assets.” Japan’s Metaplanet company has enhanced its market value through a Bitcoin treasury strategy, while more US listed companies are also rapidly following in the footsteps of MicroStrategy.

Under the general trend, cryptocurrencies are increasingly making their presence known in the global political and economic fields.

Is this a kind of “going out of the circle” that people in the coin circle often mention?

A comprehensive observation of the current trends indicates that there are mainly two paths for cryptocurrencies to break into the mainstream: the rise of stablecoins and the crypto reserves in company balance sheets.

On the surface, stablecoins provide a stable medium for payments, savings, and remittances in the crypto market, reducing volatility and promoting the widespread use of cryptocurrencies. However, its essence is an extension of dollar hegemony.

Taking USDC as an example, its issuer Circle has close ties with the U.S. government and holds a large amount of U.S. Treasury bonds as reserve assets. This not only strengthens the status of the dollar as a global reserve currency but also further extends the influence of the U.S. financial system into the global cryptocurrency market through the circulation of stablecoins.

Another way to break out is for publicly listed companies to buy coins.

Coin buying companies attract speculative funds through crypto narratives, driving up stock prices. However, aside from a few leading companies, the extent to which later imitators can improve the fundamentals of their main business, beyond just increasing market valuation, remains a mystery.

Whether it is stablecoins or cryptocurrencies being added to the balance sheets of listed companies, cryptocurrencies seem more like a tool to continue or strengthen the existing financial landscape.

Whether to cut the leek or to pursue financial innovation, it is more like looking at two sides of a coin, depending on which side of the poker table you are sitting on.

Declaration:

- This article is reproduced from [TechFlow] The copyright belongs to the original author [TechFlow] If you have any objections to the reprint, please contact Gate Learn TeamThe team will process it as quickly as possible according to the relevant procedures.

- Disclaimer: The views and opinions expressed in this article are those of the author and do not constitute any investment advice.

- The other language versions of the article are translated by the Gate Learn team, unless otherwise stated.GateUnder such circumstances, it is prohibited to copy, disseminate, or plagiarize translated articles.

Related Articles

Solana Need L2s And Appchains?

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What Is Ethereum 2.0? Understanding The Merge